NAIFA supports public policy that that promotes financial literacy, encourages Americans to prepare for their financial futures, and offers families opportunities to achieve financial security. President Christopher Gandy has spoken and written about the opportunities afforded by 530A accounts, also known as Trump Accounts. Gandy has spoken to U.S. Treasury officials about the great promise of these financial products and Treasury has asked for feedback from industry professionals. You can help us out by answering a few brief questions.

2 min read

Are You Talking to Clients About Trump Accounts?

%20(1).png)

Topics: Financial Security Federal Advocacy

2 min read

Video: Spring Is the Perfect Time to Make Your Voice Heard in Washington

NAIFA's grassroots advocacy works because our members show up. You and your colleagues come out for events like the Congressional Conference to speak to lawmakers with a unified voice on issues important to your businesses, clients, and communities. When you lend your voice, you let the people whose decisions impact your business know that the work you are doing is vital to the financial security of families and businesses in their districts across the country.

If you are a regular Congressional Conference attendee, I look forward to seeing you again May 18-19 in Washington. I urge you to invite colleagues who have never been a part of this premier grassroots event to join you. Share your experiences, and tell them how you make a difference, improve your practice, and serve the best interests of your clients at Congressional Conference. We have a limited number of $500 travel stipends available to to first-time attendees who are NAIFA members and meet other criteria.

Topics: Congressional Conference

3 min read

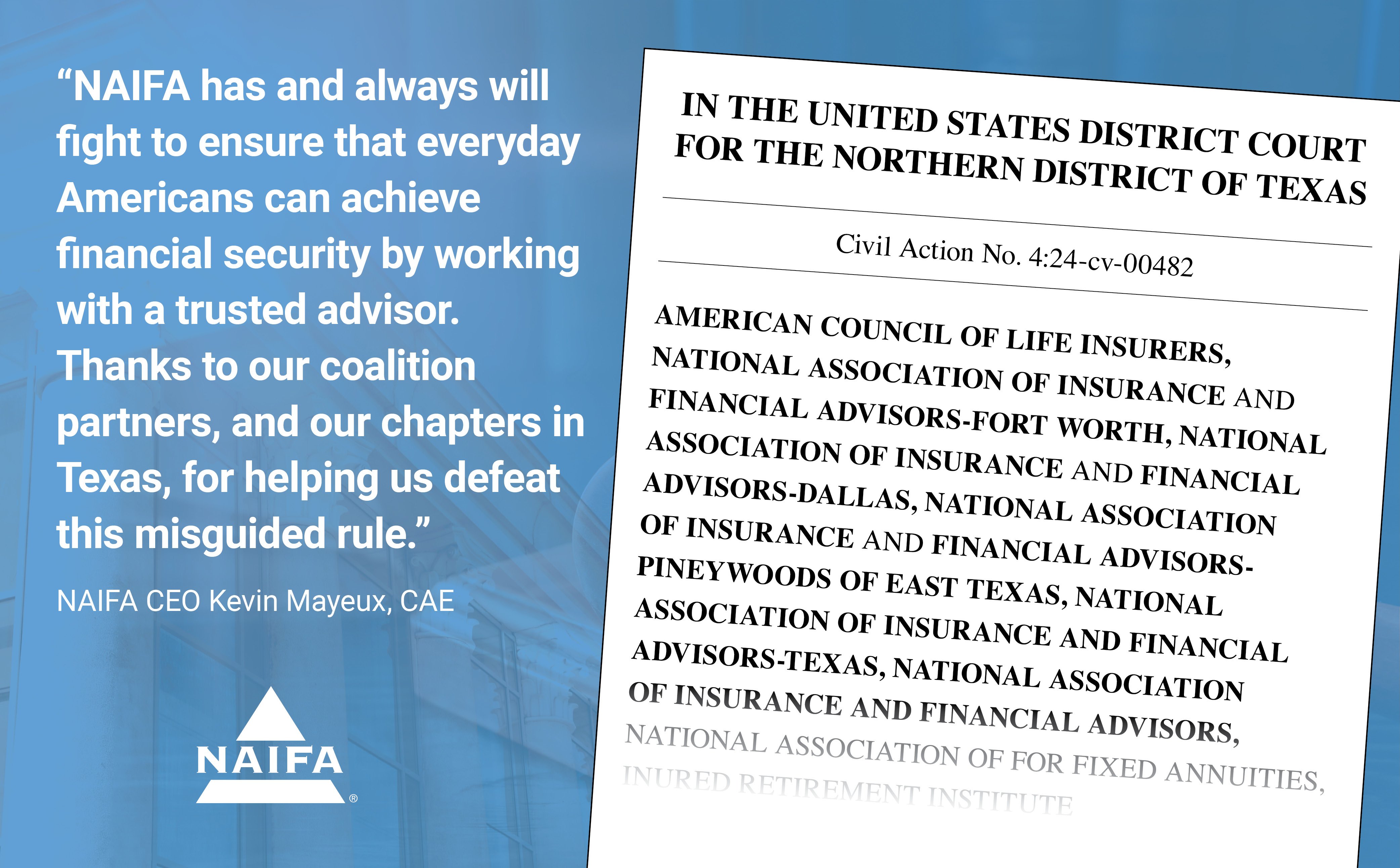

Court Vacates Fiduciary Regulation in a Win for Consumers and NAIFA Advocacy

The U.S. District Court for the Northern District of Texas issued a final judgment vacating the Department of Labor's Retirement Security Rule: Definition of and Investment Advice Fiduciary and related Prohibited Transaction Exemptions. The Texas District Court’s decision to vacate the fiduciary-only regulation is an advocacy win for NAIFA and a win for all retirement savers. NAIFA has strongly opposed the misguided regulation, which significantly would have restricted consumer choice and access to retirement advice.

Topics: Standard of Care & Consumer Protection Press Release DOL

2 min read

Utah Seeks Innovation in the State Retirement Space

For years, states have sought solutions to the growing retirement savings gap. As a result, an increasing number of states have adopted state-run auto-IRA programs, which require employers that do not offer a retirement plan to enroll their workers in a government-facilitated savings program.

Topics: State Retirement NAIFA-Utah

1 min read

NAIFA Supports the Lowering Costs for Caregivers Act

NAIFA has joined a coalition of national organizations urging Congress to pass the Lowering Costs for Caregivers Act (S.1565/H.R.138).

Topics: Limited & Extended Care Planning Center caregiving

1 min read

Register Now! The Congressional Conference Cost Goes Up on Tuesday.

NAIFA's Congressional Conference is an opportunity for financial professionals to learn to be the best grassroots advocates they can be and to stand united with fellow advisors, tell their stories directly to lawmakers, and help shape the policies that affect their practices, clients, and Main Street families across the country. Don't delay. The special early registration discount ends Tuesday, March 3. Also, if you are a first-time attendee (or would like to invite a first-time attendee), a limited number of travel stipends remain available for NAIFA members who have never attended a Congressional Conference.

Topics: Congressional Conference

1 min read

Mayeux: Protection of Financial Professionals' Independence Is Crucial in New DOL Proposal

.png)

The U.S. Department of Labor released its newly proposed independent contractor rule to determine whether workers are employees or independent contractors under the Fair Labor Standards Act (FLSA). The proposed rule, when finalized, will replace the 2024 federal rule on independent contractor classification.

NAIFA CEO Kevin Mayeux, CAE, issued the following statement:

“NAIFA is encouraged by the Department of Labor’s release of a new rule to replace the existing 2024 federal rule on independent contractor classification. The 2024 Rule fails to provide an analysis for distinguishing between independent contractors and employees under the FLSA that is sufficiently clear and leads to predictable outcomes. The 2024 Rule’s description of several economic reality factors could be viewed as setting a higher bar to find independent contractor status than required under the law. Among other harms, an analysis which is ambiguous or perceived as too restrictive of independent contracting can deter businesses from engaging with bona fide independent contractors or induce them to unnecessarily classify such individuals as employees.

Many financial advisors operate locally as small business owners, employing others on their staff, and serving the members of their communities. Reclassifying them as employees rather than independent contractors would have threated their ability to best serve their clients and to ensure that their small businesses can operate efficiently.

NAIFA is currently reviewing the proposed rule to determine the full impact on independent contractors and will remain diligent to ensure that NAIFA members are best positioned to maintain their independent business operations and to best serve their clients.

We have previously provided extensive comments and testimony to the DOL on the topic of preserving independent contractors’ rights and we now look forward to working with the department as it works to improve policies that support the independence of NAIFA members and the ability of consumers to receive professional financial guidance.”

Topics: Press Release DOL Insurance & Financial Advisor Regulation Producer Employment

2 min read

NAIFA's Gandy and Treasury Officials Discuss Trump Accounts and the Vital Role of Financial Professionals

NAIFA President Christopher Gandy along with NAIFA’s Government Relations team met with Department of the Treasury staff on February 24 to discuss the implementation and rollout of “Trump Accounts,” the newly established tax-deferred investment accounts for children under age 18 created by legislation passed last year.

Topics: Press Release Financial Security Federal Advocacy

1 min read

NAIFA Welcomes Focus on Financial Security in President's State of the Union Address

The National Association of Insurance and Financial Advisors (NAIFA) shares President Trump’s goal of helping more Americans achieve financial security and build stronger retirement savings.

Topics: Press Release Retirement Plans Trump Accounts

2 min read

NAIFA: Financial Professionals Are Essential to the Success of Trump Accounts

The National Association of Insurance and Financial Advisors (NAIFA) submitted formal comments to the Internal Revenue Service in response to Notice 2025-68 regarding the implementation of Section 530A Trump Accounts. Read NAIFA coverage in Investment News, 401kSpecialist and Advisor Magazine.