NAIFA CEO Kevin Mayeux, CAE, is among the industry leaders who signed a letter to Sens. Tim Scott (R-SC) and Elizabeth Warren (D-MA) of the Senate Committee on Banking, Housing, & Urban Affairs strongly supporting legislation to modernize federal securities regulation of 403(b) retirement plan investments by providing parity with 401(k) plans and other retirement savings arrangements.

1 min read

NAIFA's Mayeux Joins CEO Letter Urging Retirement Plan Fairness for 403(b) Participants

Topics: Retirement Planning Supported Legislation

NAIFA Supports Efforts to Expand Retirement Access

As policymakers continue to address the nation’s growing retirement savings gap, an executive action seeks to expand access to retirement savings options, particularly for workers whose employers do not offer plans. The initiative includes a new federal platform, TrumpIRA.gov, aimed at helping individuals more easily connect with existing retirement savings tools and opportunities.

Topics: Retirement Planning

2 min read

Financial Professionals Can Use Trump Accounts to Promote Financial Literacy

The IRS has reported that parents have enrolled more than 4 million American children in 530A accounts, also known as Trump Accounts. These accounts are a new type of tax-advantaged individual retirement account for children under the age of 18. Under a pilot program, the federal government gives children born between January 1, 2025, and December 31, 2028, whose parents set up accounts in their name $1,000 in seed money. Beginning July 4, 2026, parents, relatives, friends, employers, organizations, and individuals may make contributions to the plans up to annual limits. Trump accounts create opportunities for financial professionals to start conversations with consumers and clients with children about planning for the future, boosting financial literacy, and providing their children with solid financial foundations.

Topics: Retirement Planning Press Release Federal Advocacy

2 min read

NAIFA: Financial Professionals Are Essential to the Success of Trump Accounts

The National Association of Insurance and Financial Advisors (NAIFA) submitted formal comments to the Internal Revenue Service in response to Notice 2025-68 regarding the implementation of Section 530A Trump Accounts. Read NAIFA coverage in Investment News, 401kSpecialist and Advisor Magazine.

Topics: Retirement Planning Press Release 530As Trump Accounts

3 min read

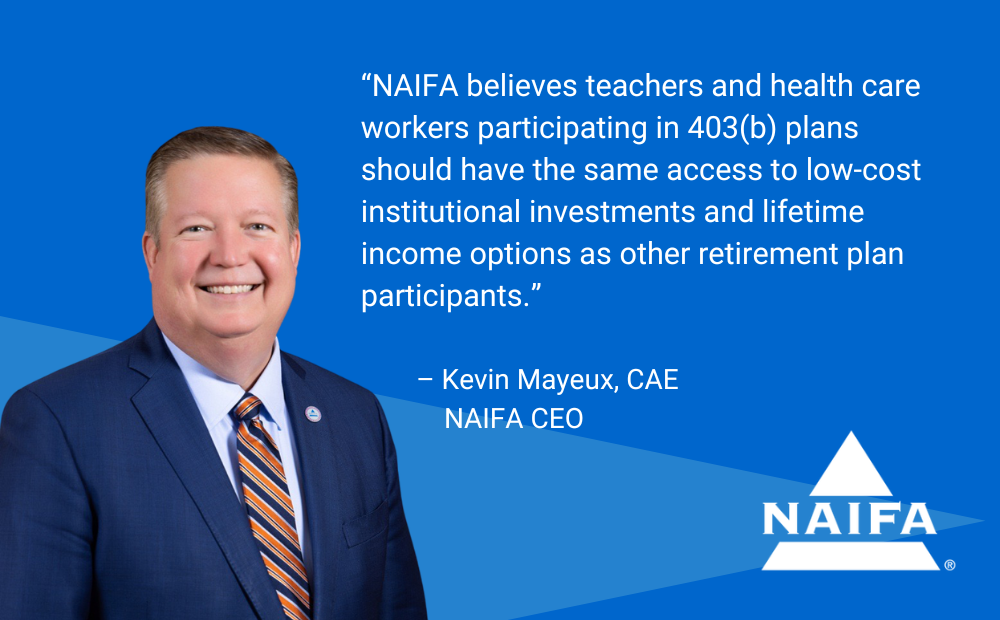

The NAIFA-Supported INVEST Act Passes the House

The bipartisan INVEST Act has passed the House of Representatives in a 302-123 vote. NAIFA supports the legislation to expand retirement-planning options for teachers, employees of nonprofit organizations, and others.

"NAIFA is pleased to see the House take bipartisan action to bolster the ability of more Americans to better prepare for retirement," said NAIFA CEO Kevin Mayeux, CAE. "The INVEST Act would give teachers, hospital workers, nonprofit employees, and others who have 403(b) plans access to expanded investment options, including annuity-linked products that provide guaranteed lifetime income. It would also take steps toward addressing elder financial exploitation and would remove unfair impediments that prevent expert investors who don't meet net-worth thresholds from taking advantage of some sophisticated investments."

Four sections of the bill are particularly noteworthy to financial professionals and their clients.

Topics: Retirement Planning Press Release Supported Legislation

1 min read

NAIFA-Supported Bill Would Expand Retirement Planning Options for Teachers and Employees of Non-Profits

NAIFA CEO Kevin Mayeux, CAE, issued the following statement on the bipartisan INVEST Act:

Topics: Retirement Planning Press Release Supported Legislation

1 min read

DOL Advances Fiduciary-Only Proposal That Would Limit Access to Financial Services for Lower- and Middle-Income Consumers

.png)

NAIFA CEO Kevin Mayeux, CAE, issued the following statement in response to the U.S. Department of Labor’s decision to advance its proposed “Retirement Security Rule” for review by the White House Office of Management and Budget (OMB).

Topics: Retirement Planning Legislation & Regulations Standard of Care & Consumer Protection Press Release DOL

2 min read

NAIFA-WA Testifies at Hearing on State-Run Retirement Legislation

NAIFA members in Washington state and across the country have dedicated their careers to ensuring their clients are well-prepared for retirement. Financial professionals offer a robust variety of products and services, working with employers and employees, alike, to provide retirement security options.

Topics: Retirement Planning State-Facilitated Retirement Plans Opposed Legislation Washington

3 min read

NAIFA Thanks Lawmakers Asking DOL to Withdraw Its Fiduciary-Only Proposal

NAIFA appreciates the work of a bipartisan group of federal lawmakers who oppose the Department of Labor’s proposed “Retirement Security” rule that would require a fiduciary-only model for financial services.

Representatives French Hill (R-AR) and David Scott (D-GA) and forty-eight of their colleagues in the House signed a letter to acting DOL Secretary Julie Su and Assistant Secretary Lisa Gomez asking the Department to withdraw its proposal.

Topics: Retirement Planning Legislation & Regulations Standard of Care & Consumer Protection DOL

3 min read

NAIFA Survey Shows the DOL’s Fiduciary Proposal Will Increase Costs and Reduce Access to Retirement Planning Services

NAIFA conducted a survey of more than 1,000 members between November 27 and December 1, 2023, to gauge the potential effects of the U.S. Department of Labor’s proposed “Retirement Security Rule: Definition of an Investment Advice Fiduciary” on the consumers who rely on financial professionals for retirement products, services, and advice.